To Buy or Not To Buy A Home in Colorado Springs–That is the Question!

There are a number of reasons that buying a home provides more advantages than renting. From gaining equity and wealth, to simply being in control of your living situation, buying a home can set your family up for success.

Rising Rent Prices

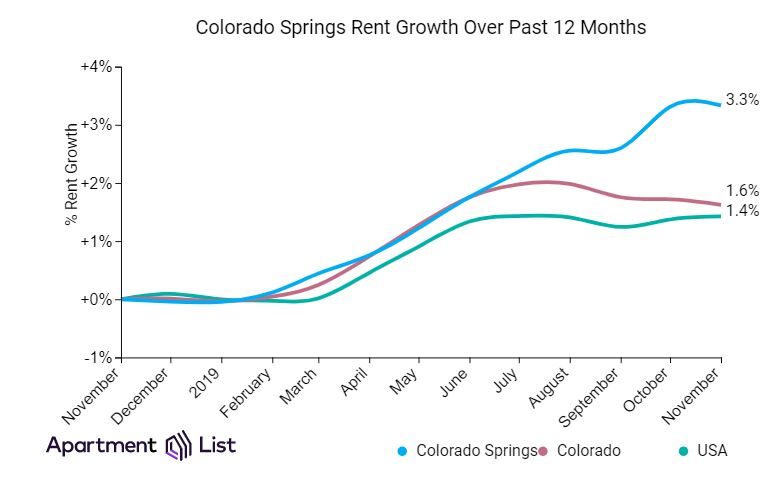

Did you know that here in Colorado Springs, the average rent has been increasing every year?

According to one study, “Colorado Springs rents have increased by 3.3% year-over-year, well over the state average of 1.6%, as well as the national average of 1.4%.”

This means that every time your lease renews, your rent is likely to increase and you are going to be paying more for the same home. When you own your home, your mortgage payment remains the same each year, providing financial stability (property taxes and homeowners insurance may vary slightly each year, but the principal payment should not).

According to a Zillow Report, “The U.S. median rent now consumes 27.8% of the country’s median income – nearing the 30% tipping point above which rent is considered unaffordable and the 32% tipping point above which communities can expect a more rapid increase in homelessness.” In addition, “renters are financially strapped enough that only 51% say they could accommodate a $1,000 expense, compared to 80% of homeowners”.

Changes in rent can wreak havoc on a budget, especially if you are already renting at the top of your budget.

Wealth and Equity

When you rent a home, you are essentially still paying a mortgage– just someone else’s and not your own! You pay the mortgage without the possibility of ever owning the property or gaining any personal equity.

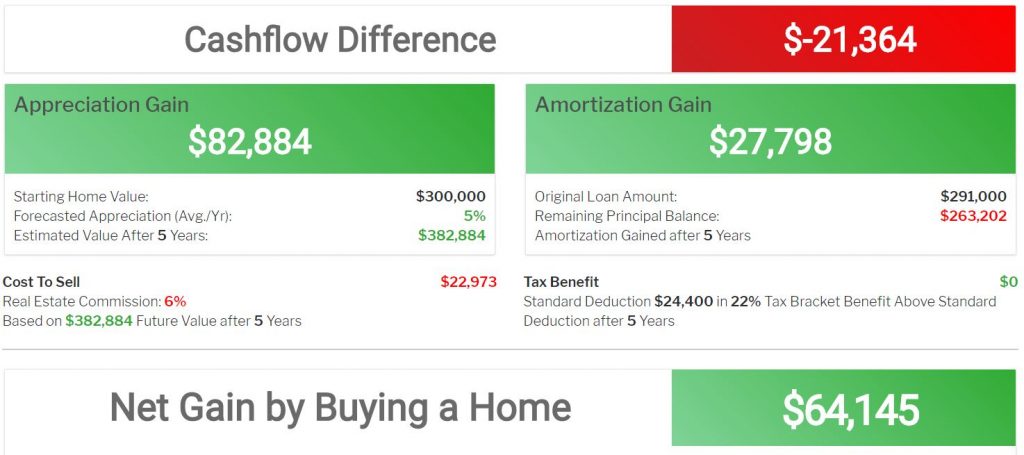

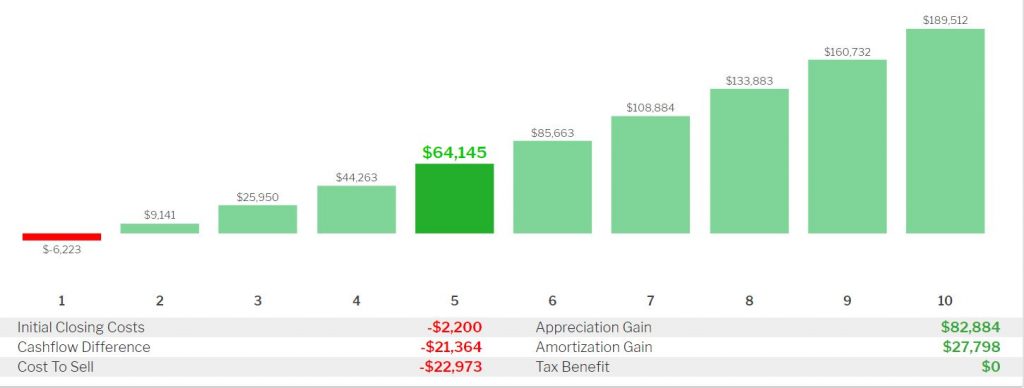

John Haney of Colorado Mortgage Company shows the difference in equity in owning vs renting over a 5 year time frame.

As you can see, there are advantages to being a homeowner as well as a consistency in the mortgage payment (whereas rents will rise). A homeowner of a $300,000 home (3% down payment) will have an approximate appreciation gain of $82,884 after 5 years and an equity gain of $27,798, whereas a renter will not have any net gains. (Read below for more information on appreciation) This means that the home will be worth roughly $82,884 more and the owner will have paid off $27,798 in principal for a gain of $110,682 in 5 years!

Every three years, the Federal Reserve conducts its Survey of Consumer Finances. Data is collected across all economic and social groups. The latest survey data covers 2013-2016.

The study revealed that the median net worth of a homeowner is $231,400 – a 15% increase since 2013. At the same time, the median net worth of renters decreased by 5% ($5,200 today compared to $5,500 in 2013). These numbers reveal that the net worth of a homeowner is over 44 times greater than that of a renter.

While there may be some costs associated with owning a home, the wealth you will build often outweighs those costs.

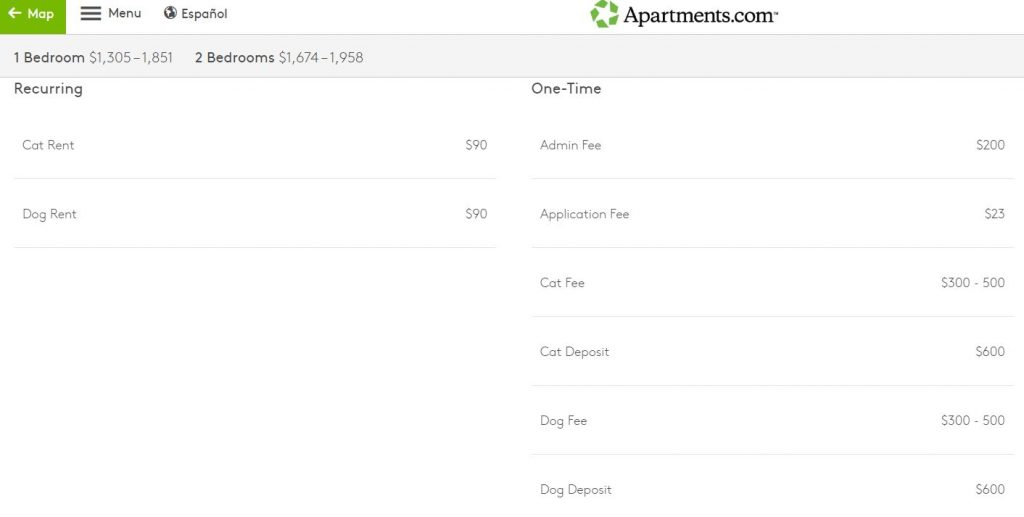

Fees and Deposits

When renting, there are a variety of fees that go along with it. For example, there are application fees (typically $50 per applicant) to apply for a rental. In addition, there is often a security deposit equal to one month’s rent required up front. There are also pet deposits and pet rent. See the image below for an idea of how much those fees can run. As a homeowner, there are no fees associated with pets and no one can dictate which breed of animals you can have. This means that a renter will need several thousand dollars up front just to move into a rental. Did you know there are home buying programs that can allow you to move into a home with as little as $1,000 down?! Moving into a rental could cost you more than simply buying a home!

Moving

As a renter, you are subject to the terms of your lease. Often times, you may be forced to move if the landlord does not want to renew the lease, decides to sell the property, or chooses to move back in. This may force your family to scramble to find a new place to live with as little as 30 days notice. In turn, you will have to come up with a new set of deposits and fees to apply for a new rental.

Modifications

Do you love decorating your home and making it your own? As a renter, there are many modifications that you may not be able to do. For example, changing paint colors, flooring, fixtures and other changes might not be allowed per your lease. Your options for landscaping and gardening may also be limited, and doing any modifications on a home that is not yours will only benefit the landlord, not you. Renting can make you feel like you are living in someone else’s home and not your own.

Restrictions and Rules

Did you know that when renting there are often numerous rules you must abide by? For example, most landlords do not allow smoking (of any kind) on the property. Also, you may have a limit as to how long guests can stay without approval. This means that if you would like family to visit for an extended period, you might need approval from your landlord, whereas if you owned your home, you could control how long someone may visit. Pet and breed restrictions often apply when renting– and in case you didn’t already know, the list of rentals decreases substantially when you have pets, especially if you have more than one!

Repairs

Renters typically rely on their landlord for repairs. While this can save money for some renters, it can also be a nightmare. There are stipulations stating what a landlord is responsible for and what they are not. In non-emergency cases, a landlord does not have to complete repairs immediately. Even emergency repairs can be a headache, especially if the landlord is unreachable to approve the repair. Not every repair is the responsibility of the landlord– for example, in some leases the repair of the dishwasher or disposal is not considered necessary, and thus will fall onto the renter.

Appreciation

Homes have been greatly appreciating here in Colorado Springs. This means the same home will cost you more to buy next year versus buying it today. As John Haney’s example shows with an estimated appreciation of 5% per year, a $300,000 home will likely be worth $315,000 just one year later. After 5 years, it could be worth $382,884 or more!

Even with a more conservative example of 3% annual appreciation, a $300,000 home would be worth approximately $347,782 after 5 years! In either situation, the homeowner is still gaining wealth!

Colorado Springs has typically been seeing high appreciation, although this is not always indicative of future appreciation (closer to 6%-7% year over year). Every month we pull the real estate statistics for the Pikes Peak Region. For example, the average price of a home went up 6.6% and the median price went up 7.3% in November 2019 compared to November 2018. As you can see, waiting another year to buy could cost you thousands!

Interest Rates

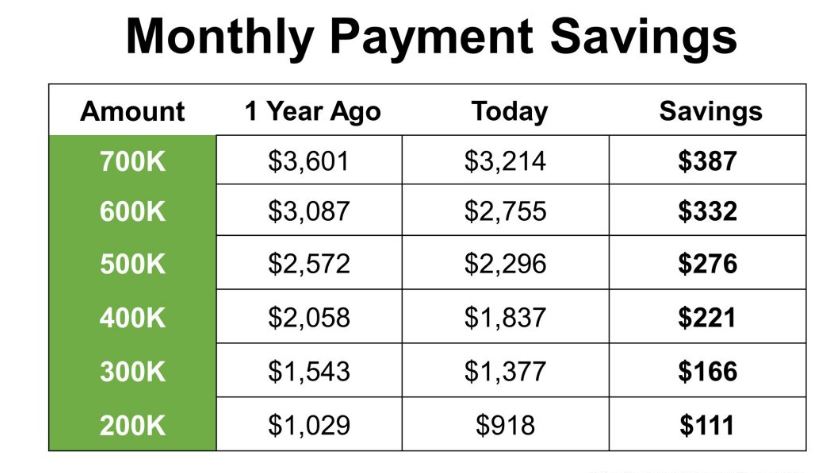

Currently, interest rates are very low, even compared to this time last year. Lower interest rates give the buyer more purchasing power allowing them to afford more home. Waiting can cost you if interest rates begin to rise again. This means that as interest rates rise, you will have to buy a cheaper house to keep the same payment. Buying while rates are low will allow you to have a higher budget for the home itself. To see how interest rates can impact your monthly payment, check out the chart below by KCM.

Colorado Springs Market Predictions

According to the National Association of Realtors (NAR), Colorado Springs was identified as #3 on the top metro areas for the next 3-5 years. This study was based on “domestic migration, housing affordability for new residents, consistent job growth relative to the national average, population age structure, attractiveness for retirees and home price appreciation, among other variables”.

In another study, Colorado Springs was ranked as the #1 housing market to watch.

Colorado Springs was also ranked as the #2 Best Place to Live by US News and World Report.

Are you ready to buy?

If you are thinking about buying a home here in Colorado Springs, please don’t wait. Reach out to our team and we can help you get started! Even if you don’t think you are in a position financially to buy right now, please reach out to John Haney and his team can help put you on the path to home ownership! You do not need 20% down to buy a home and you don’t need a 750 credit score! Let us help you find your dream home today!

vanwierenrick@gmail.com

Mary Barkley (719) 421-9360

mbarkley.9360@gmail.com

john@coloradomortgage.company

www.coloradomortgage.company

Pingback: 2022 BAH Rates for Fort Carson - Living Colorado Springs

Pingback: Rentals in Colorado Springs - oldfarmnews.com

Pingback: Rentals in Colorado Springs - Living Colorado Springs

Pingback: Migration and Rental Trends in Colorado Springs - Living Colorado Springs

Pingback: 2021 BAH Rates Fort Carson - Living Colorado Springs