Home Equity Conversion Mortgage

Do you need more cash in your pocket during retirement years? Have you heard of a home equity conversion mortgage (HECM)? If not, this is the article for you (or maybe a loved one you know!).

A home equity conversion mortgage allows a homeowner to tap into some of the equity in their home. It allows the owner to have no mortgage payments, but also have money to live off of. All too often seniors are finding it increasingly difficult to afford medications, utilities, groceries, etc. and the HECM will allow seniors to live more comfortably without giving up their home.

This may sound eerily familiar to a reverse mortgage, but there’s some key distinctions for a HECM. It is not as scary as you may think!

A Home Equity Conversion Mortgage:

- Owner does NOT give up title

- Lender does NOT take ownership

- Does NOT incur debt that is passed onto heirs

- Owner can NEVER owe more than the value of the home

- No other asset used/required

- Owner will not have to move or sell

- Owner does not have to use ALL of their equity

- Zero impact on Social Security or Medicare

- Minimal out of pocket

- Closing costs similar to a traditional mortgage

It’s important to point out that owners will not give up ownership of their home if using this program. Additionally, a HECM is not always used for those who need extra cash; it can also be a good option for some seniors to avoid drawing on taxable assets. (The equity in your home is not taxable).

While some may think, why use up your equity? Well, for those that have over 50% equity in their homes, this can be a cheaper way to have some much needed income rather than taking out a personal loan or racking up credit cards. It can also help seniors have more liquid assets or use that money in higher income-producing ways. Whatever the reason, it can be a useful tool as part of a financial strategy!

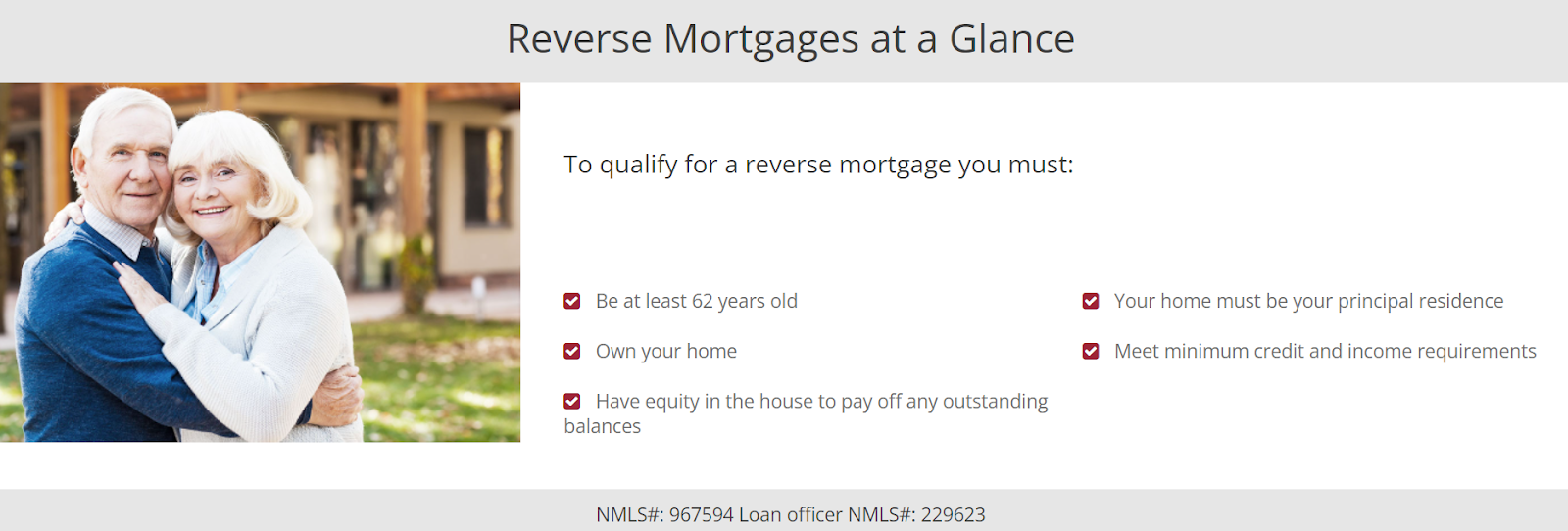

The older you are when you apply for this program, the less money down required. The loan size is also dependent on age and interest rate. You must be 62 years old for an FHA HECM (insurance included) or 55 years old for a conventional. You will need slightly more than 50% equity in your home to qualify. There is a one-time interest payment at the end, but a 1098 will be generated which can help lower estate tax.

Additionally, there is a way to use a HECM to purchase a home. This applies to those seniors that have a large amount of cash to put down, but can essentially eliminate a mortgage payment altogether.

There are only a few instances when repayment will be called due. These circumstances include:

- The house must remain your primary residence

- If you default on taxes or insurance (if you don’t have an escrow acct)

- Turning age 150

- If you transfer title (revocable trust is okay)

It’s important to talk to a reputable, local lender and a tax professional to see if this program is right for your personal situation. John Haney of Colorado Mortgage Company is an expert on this program and can easily answer your questions regarding home equity conversion mortgages.

Questions? Please contact us! We would love to help!

Some common myths (according to myhecm.com)

- Myth#1: “I’m giving up ownership of my home.”

Not at all. A reverse mortgage is fundamentally just a home loan, but one designed to give you access to your equity without you having to give up ownership of the home or take on a monthly mortgage payment. Like a traditional forward mortgage, you always retain title ownership of the home. You are not selling your home to the bank when you get a reverse mortgage.

- Myth #2: “The reverse mortgage is just a loan of last resort for broke and desperate people.”

Not at all. In fact, many so-called broke or desperate people often don’t even qualify for a reverse mortgage. Many very well-off people get reverse mortgages for a variety of reasons, including supplementing income, increasing liquid assets, extending the life of their assets, minimizing income taxes, and gaining additional financial flexibility in retirement. A reverse mortgage can be a great addition to an already solid financial plan for retirement.

- Myth #3: “The reverse mortgage will use up all of my equity.”

Not necessarily. It’s true that a reverse mortgage is designed to convert equity into cash, which means your loan balance rises over time. However, it’s also designed to preserve equity. It’s not a financially viable program if it uses up your equity quickly.

A HECM reverse mortgage is a non-recourse loan insured by FHA. This means the FHA insurance fund covers the shortage if there’s not enough value in your home to settle the entire loan balance at the time of repayment. For the program to be financially viable, it has to be designed in such a way as to limit the claims against the insurance fund, which means it has to preserve equity at the same time it gives you access to your equity.

It’s also important to understand that you often have a lot of latitude to decide how much of the reverse mortgage proceeds you use. If you use less, then more of your equity is preserved for longer. If you use more of the proceeds, then you’ll use up your equity faster.

- Myth #4: “I’ll be passing on a big debt to my heirs.”

Again, the reverse mortgage is a non-recourse loan insured by FHA, which means that a debt can never be passed on to your heirs. If there’s not enough value in the home to pay off the entire balance, you or your heirs are not responsible to cover the shortage. The most that has to be paid back is the value of the home at the time the loan is due and payable.

- Myth #5: “Reverse mortgage interest rates are sky high.”

Not at all. In fact, HECM reverse mortgage rates are often very comparable to traditional mortgage rates. This is possible because FHA insures the loan, which reduces risk for the lender. Therefore, lenders can offer very attractive interest rates on reverse mortgages.

- Myth #6: “The fees are really expensive.”

This is true sometimes, but not all the time. If you live in a high value home and you’re paying off a large mortgage balance, it’s possible the fees could be pretty stiff because of the IMIP charged by FHA. However, lenders often have some leeway to chop or eliminate their origination fee and/or cover third party fees because of the larger loan amount.

On the other hand, if your home is less expensive and you have little to no mortgage balance to pay off, your closing costs could be very comparable to a traditional forward mortgage.

- Myth #7: “The bank takes my house when I die.”

Not at all. You are always the owner and you’re free to leave the home to whomever you wish. If your heirs wish to keep the home, they need to either pay off or refinance the reverse mortgage balance. If they don’t wish to keep the home, then the bank can step in, sell the home, and pay back the reverse mortgage balance. Any remaining equity goes into your estate and to your heirs.

- Myth #8: “I can’t take any long trips or temporarily go into a nursing home or I might lose my house.”

Not at all. Yes, you need to live in the home, but it doesn’t mean you can’t take a long trip or stay in a nursing home for a few months. As long as you live in the home at least part of the year and it remains your primary residence (not a second home or rental), you have met the residency requirements of the program.

- Myth #9: “I can’t ever sell my house. I’m locked in for the rest of my life.”

Not at all. The reverse mortgage is better suited for people who don’t plan to sell anytime soon. However, if circumstances change and you need to sell, you can. You simply sell the home, pay off the balance with the proceeds of the sale, and the remaining equity is yours to keep.

The reverse mortgage also has no prepayment penalty.

- Myth #10: “As long as I’m 62 and have equity in my home, I qualify for a HECM reverse mortgage.”

Unfortunately, it’s not quite that simple. There’s more to qualifying than just having equity in your home and being at least 62. Today, lenders have to evaluate your income and credit through a process called financial assessment and the home has to be in at least reasonably good condition for you to qualify. Not everybody who owns a home and is 62 or older can get a reverse mortgage.

- Myth #11: “I don’t need it now. I can just wait and get a reverse mortgage when I really need it.”

Don’t count on it. It’s actually gotten tougher to get a reverse mortgage over recent years. FHA has tightened the qualifying standards to reduce defaults due to nonpayment of property charges (property taxes, homeowner’s insurance, HOA dues, etc.). Just because a reverse mortgage is available to you today doesn’t mean it will be tomorrow. Even if guidelines don’t change at all, plenty of other factors could make a reverse mortgage less workable or attractive for you in the future:

- Higher interest rates – A reverse mortgage offers more money when rates are lower. If rates rise in the future, you may not qualify for as much money as you can today.

- Lower property values – Many real estate markets across the country have seen big increases in home values over recent years. If you’re in one of those places, your market could be ripe for a correction. If home values fall, you may not qualify for as much money.

- Deterioration in your credit or financial profile – FHA rolled out new financial assessment guidelines in 2014 that require lenders to take into account your income, expenses, and credit history. If you take on a lot of debt or incur big medical bills, you may have difficulty qualifying.

- Deterioration in the condition of your home – We all know that homes take maintenance over time. If you’re tight financially and can’t keep up with the maintenance of your home, it may be tough to get a reverse mortgage in the future. Your home doesn’t need to be perfect, but it does need to be in at least reasonably decent shape to qualify for a reverse mortgage.